Of all the adjustments that turn a practice’s P&L into a valuation, one moves the number more than any other, and it is the one do-it-yourself tools most reliably get wrong: normalizing owner compensation. I touched on it in the add-backs piece. Here is the full picture, because if you get only one adjustment right, make it this one.

What it actually is

As a producing owner, the compensation on your books blends two different things a buyer separates. Part of it is the clinical wage you earn for the dentistry you personally do. The rest is the profit you keep because you own the practice. A buyer needs to know how much of your pay is wage and how much is owner profit, because only the profit travels with the business.

The two steps

Normalizing owner comp is a two-step move. First, you add back everything the practice pays you: your W-2 salary plus the benefits that run through the practice on your behalf, such as health insurance, retirement contributions, and the payroll taxes on your compensation. Second, you subtract the market-rate cost of replacing your clinical production, because a buyer has to pay a real dentist to do the work you do today.

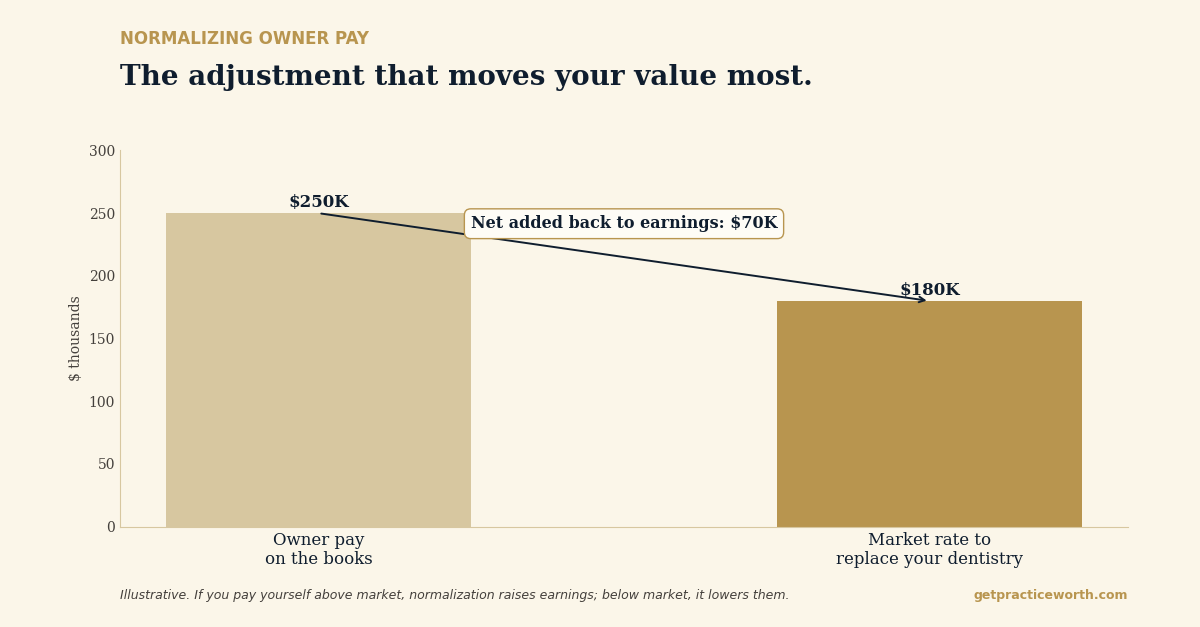

Here it is with round numbers. Say you pay yourself 250,000 dollars, but the market rate to replace the dentistry you personally produce is 180,000. The 70,000 dollar difference flows back into earnings.

That single adjustment, before any other add-back, can move your valuation by six figures.

The direction surprises people

If you pay yourself above market, normalization raises your adjusted EBITDA and your value. If you pay yourself below market, which is common among owners who keep salary low for tax reasons, it lowers your adjusted EBITDA. A lot of owners are surprised by that second case. Paying yourself a small salary feels efficient, but to a buyer it understates the cost of running the practice, because they still have to pay a dentist a real market wage. Once that is corrected, the number comes down.

Multiple owners and associates

In a multi-owner or multi-provider practice, this is done for each clinician separately. W-2 associates already paid at market usually need no adjustment. An owner-partner gets the same two-step treatment you do. A 1099 contractor producing outside the practice books is handled at their own replacement rate. Miss one of these providers and the whole valuation tilts.

Why the free tools get it wrong

When we ran a real practice through ChatGPT, it skipped both halves of this adjustment entirely. It never added back the owner’s compensation and never subtracted a replacement cost, a swing of hundreds of thousands of dollars, and it did so with complete confidence. Owner-comp normalization is not an optional refinement. It is the core of the work, and it has to be done with real replacement rates, not a guess.

This single adjustment is why two practices with identical profit on paper can be worth very different amounts. Get it right first, then worry about the rest. Practice Worth has you set your own compensation and models the replacement cost for you, so this adjustment is built correctly before anything else is layered on. There is a free sample report at getpracticeworth.com.

About the author. Dr. David Eslinger holds a DDS and an MBA and has spent more than a decade on the buy side of dental practice transactions, founding Eslinger Dental Consultants and holding C-suite, executive leadership, and board roles in the DSO industry. Karen Eslinger, RDH, co-founded Practice Worth in 2026. Practice Worth is a Missouri LLC. Learn more at getpracticeworth.com.

Karen’s companion piece takes on the second half of the adjustment: what a replacement dentist really costs.