I’m a dentist by training with an MBA, and I’ve spent most of my career around dental practice valuation, more recently on the buy-side helping DSOs and PE-backed groups evaluate acquisitions. When my wife Karen and I built Practice Worth, a self-serve dental practice valuation tool, I wanted to know one thing before we launched: how does our work compare to what a dentist would get from ChatGPT?

ChatGPT is the easy first stop. It costs nothing, the answer comes back in seconds, and the tone of the response sounds authoritative. If a dentist can get a reasonable valuation out of ChatGPT in five minutes, we have no business charging for ours.

So earlier this month, we ran the experiment. Two realistic dental practice scenarios. We uploaded the same P&L and Collections by Provider report to both ChatGPT and Practice Worth, asked ChatGPT to calculate adjusted EBITDA and apply a market multiple, and logged what came back.

What we found was worse than I expected, and the failure pattern is the part every practice owner should pay attention to.

Test 1: A single-doctor GP practice

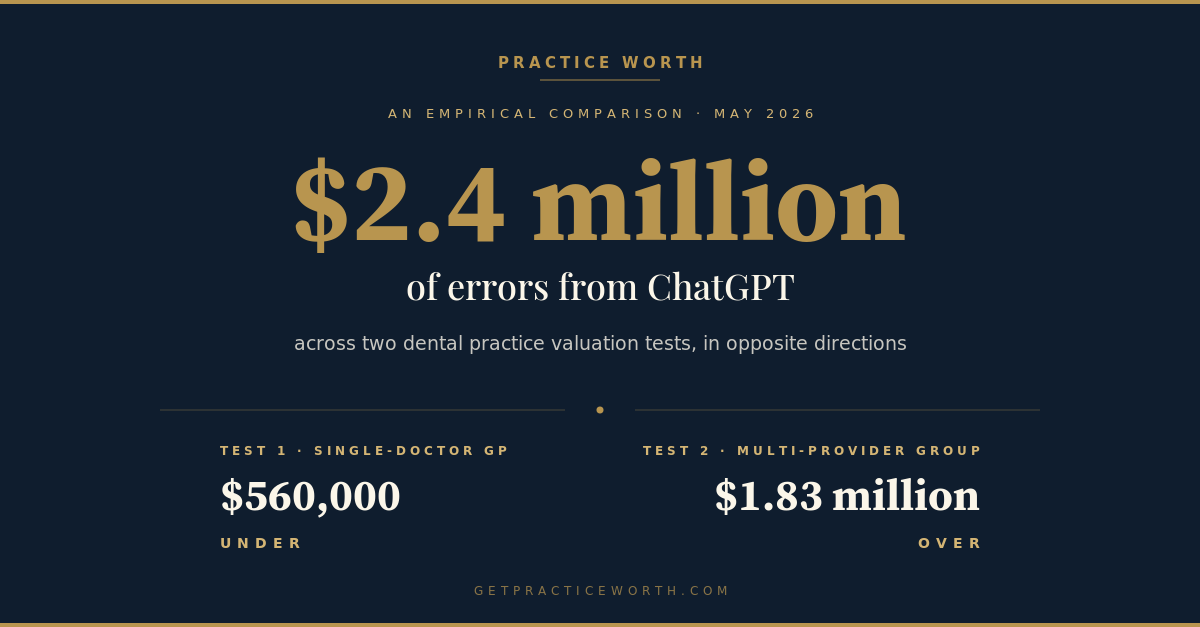

The first test was a classic owner-operator scenario. One dentist, one hygienist, $1.2M in collections, $289K net income on the P&L. The kind of practice most U.S. general dentists own.

ChatGPT produced an adjusted EBITDA of $280,300 and a midpoint valuation around $1.4 million.

Practice Worth produced an adjusted EBITDA of $392,561 and a market-multiple midpoint of $1.96 million.

Gap at the midpoint: $560,000. ChatGPT undervalued the practice by more than half a million dollars.

When I asked ChatGPT how confident it was in its number, it said it was “reasonably confident based on adjusted EBITDA and typical dental practice multiples.” That sentence is the part that concerns me. The number was wrong, and the tool had no idea it was wrong.

Here is what ChatGPT actually missed on that single-doctor practice, all of it visible on the P&L it had been given:

- It read net income as $268,300 instead of $289,260. A simple OCR error before any methodology was applied.

- It missed depreciation entirely. The line item said “Depreciation Expense $30,000.00,” clearly labeled. ChatGPT said “if not explicitly stated, you would need to adjust separately.” It was stated.

- It missed amortization entirely. Same pattern. $6,000 unread.

- It performed no owner compensation normalization at all. In dental valuation, you add back what the owner pays themselves and subtract what it would cost to replace them with a market-rate dentist. ChatGPT skipped both halves. Total owner comp adjustment Practice Worth applied: $292,200 in add-backs offset by $270,000 in replacement comp.

- It missed every discretionary add-back. Continuing education, auto, cell phone, meals and entertainment, charitable contributions. $33,101 in total, none of it captured.

Any one of those is a meaningful error in a practice sale negotiation. Together they produced a number that would have cost the owner $560,000 if they had walked into a real conversation using it.

Test 2: A multi-provider group practice

The second test was more complex, the kind of practice a DSO or PE-backed group buyer is actively looking for. Two owner-partners, two W-2 associates, one outside-P&L 1099 contractor, three hygienists, $3.5M in collections. This is what I see almost every week on the buy side of my consulting work.

ChatGPT produced an adjusted EBITDA of $1,060,000 and used a 3x to 6x multiple range, landing on a midpoint valuation around $4.77 million.

Practice Worth produced an adjusted EBITDA of $489,747 and used a 4x to 8x at-scale group buyer multiple range, landing on a market-multiple midpoint of $2.94 million.

Gap at the midpoint: $1,831,521 too high. ChatGPT overvalued the same multi-provider practice by more than $1.8 million.

This one would have been arguably worse for the seller than the undervaluation in Test 1. A practice owner walking into a buyer conversation asking $4.8 million for a practice worth $2.9 million is going to lose the deal. Buyers walk away, the seller’s credibility for any subsequent conversation is damaged, and the transaction collapses before it reaches a Letter of Intent.

Here is what ChatGPT missed on the multi-provider test:

- OCR errors on multiple line items. The worst one: it read depreciation as $8,000 when the actual figure on the P&L was $80,000. An entire digit dropped.

- It omitted around $273,700 in expense line items from its analysis. Associate doctor pay ($144,000), utilities, continuing education ($28,000), equipment lease ($24,000), workers comp insurance, and others. All clearly listed on the P&L.

- It didn’t identify the outside-P&L 1099 contractor at all. An oral surgeon producing $380,000 in collections paid through a 1099 arrangement outside the practice books. This required a $190,000 replacement compensation adjustment in Practice Worth. ChatGPT didn’t mention the provider once.

- It didn’t connect W-2 associate collections to the Associate Doctor Pay expense line. Two of the providers on the collections report appeared nowhere in the expense analysis.

- It applied the wrong multiple tier. It used 3x to 6x, the typical range for sub-$2M owner-operator practices. The correct tier for an at-scale group practice with multiple providers and DSO-buyer interest is 4x to 8x. Wrong multiple on wrong EBITDA produces wrong valuation twice.

The pattern that worries me most

If both tests had been off in the same direction, a practice owner could write themselves a mental correction. “ChatGPT is conservative; add 30%.” Or “ChatGPT is aggressive; subtract 20%.”

But the errors went in opposite directions. ChatGPT undervalued the simpler single-doctor practice by $560,000, then overvalued the more complex multi-provider practice by $1.83 million. That is roughly $2.4 million of error across two test cases, with no way for the dentist running the tool to know in advance which direction it is going to lean.

This is the core problem. A practice owner using ChatGPT for a valuation has no way to self-correct. They don’t see the mistakes the tool is making (depreciation dropped, 1099 contractor invisible, owner compensation never normalized) because the tool sounds authoritative either way. The answer can land anywhere from catastrophically low to catastrophically high depending on the complexity of the practice.

In my buy-side consulting work, I’ve sat across the table from sellers who arrived with valuations they relied on from sources they trusted. When the number doesn’t survive a quality-of-earnings review, the deal either dies or gets restructured at terms much worse than the seller expected. Either way, the work the owner did over twenty or thirty years gets priced by someone else, on someone else’s terms.

What this means if you’re thinking about selling

Two things to take from this experiment.

First, don’t use a generalist AI tool for a dental practice valuation. The problem isn’t that ChatGPT is bad at general work. The problem is that dental valuation has specific conventions (owner compensation normalization, replacement doctor compensation, discretionary add-backs, specialty-specific multiple tiers, 1099-versus-W-2 provider handling) that a generalist model doesn’t reliably apply. The two tests above demonstrate this directly. The errors are not edge cases. They are the basic mechanics of the work.

Second, recognize that the choice in front of you is not “free AI tool” versus “$5,000 certified appraisal.” There’s a middle. There has been a hole in the dental valuation market for years: dentists who need a defensible, DSO-grade number to negotiate with, plan around, or compare offers against, but who don’t have a bank-loan or legal reason to spend $5,000 and wait three weeks for a USPAP-certified appraisal.

That middle is what Karen and I built Practice Worth to fill. The wizard takes about ten minutes, covers sixteen-plus add-back categories, models replacement doctor compensation, applies specialty-specific multiple tiers, and handles multi-location and group practice scenarios. The output is a defensible PDF report that shows its math at every step, so you can hand it to your CPA or your buyer and they can see exactly how the number was built.

We validated the methodology against a 25-scenario internal test bench, ranging from single-doctor GPs to multi-location DSO-acquisition targets, before we opened it to paying customers. In our most rigorous full-detail tests, Practice Worth’s automated output matched our hand-computed expected EBITDA to the dollar.

If your situation requires a USPAP-compliant appraisal (bank financing, litigation, partnership disputes) you still need a certified appraiser. Practice Worth is the middle tier of this market. The top tier is occupied by free broker calculators, which are cheap and fast but explicitly ballpark by their own disclosure. The bottom tier is occupied by USPAP-certified appraisers, which are formal but cost several thousand dollars and take weeks. Practice Worth fills the space between.

The honest takeaway

ChatGPT is a remarkable tool for many things. Valuing your dental practice is not one of them right now. The level of precision a real transaction requires is not there yet.

If you’re a dentist thinking about selling, partnering, or just want to understand what your practice is worth before any of that becomes urgent, the number you’re working from should come from a tool built for the work. The empirical data from these two tests should make the choice clear.

If you want to see what a self-serve DSO-grade valuation looks like, we have a free sample report at getpracticeworth.com. The full product is $99 under our launch pricing.

Either way, please don’t walk into the biggest transaction of your career with a number ChatGPT made up.

About the author. Dr. David Eslinger holds a DDS and an MBA and has spent more than fifteen years on the buy side of dental practice transactions, working with DSOs and PE-backed dental groups to evaluate acquisition targets. Karen Eslinger, RDH, co-founded Practice Worth in 2026. Practice Worth is a Missouri LLC. Learn more at getpracticeworth.com.

For the full side-by-side numbers from both tests, see the detailed empirical comparison page.