If you are going to plan around what your practice is worth, there is one term worth understanding well, because every serious buyer uses it and most owners have never had it explained plainly. The term is EBITDA, and the version that matters is adjusted EBITDA.

What EBITDA is

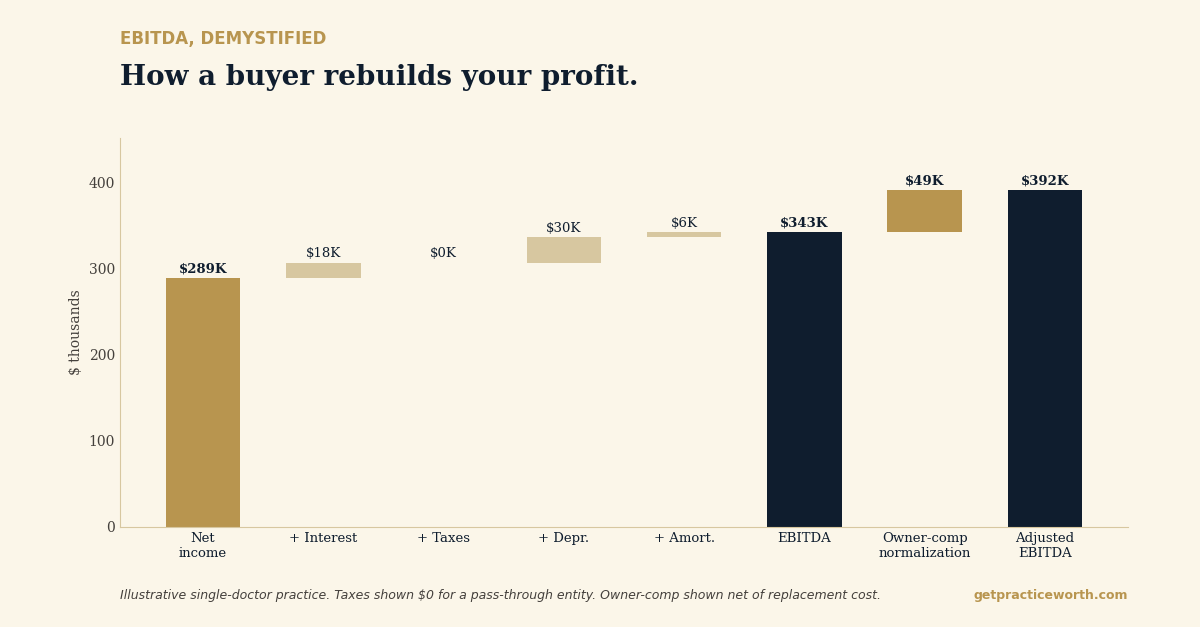

EBITDA stands for earnings before interest, taxes, depreciation, and amortization. In plain language, it is an attempt to measure the true operating profit of the practice, stripped of choices that are specific to the current owner’s financing and accounting. The net income at the bottom of your P&L is not that number. It is shaped by how much debt you carry, how your accountant handles depreciation, and a dozen other decisions a new owner would make differently.

So a buyer rebuilds it. They start from your reported net income and add back the items that are not part of the practice’s core operating profit.

The rebuild, step by step

Picture a single-doctor practice with 289,000 dollars of net income on the P&L. A buyer adds back interest expense on practice debt, because the new owner will finance the practice their own way. They add back depreciation and amortization, which are non-cash accounting entries rather than real operating costs. For a pass-through practice, income taxes are handled at the owner level, so there is typically nothing to add there.

Those add-backs alone might lift that 289,000 to roughly 343,000 dollars. That is the practice’s EBITDA.

From EBITDA to ADJUSTED EBITDA

EBITDA is not the finish line. The most important adjustment in dental valuation comes next: normalizing owner compensation. A buyer needs someone to do the dentistry you currently do, and that person has to be paid at market rate. So the buyer adds back what you pay yourself and subtracts what it would cost to replace your clinical production. They also add back discretionary spending that runs through the practice but would not transfer, such as a personal vehicle, continuing-education travel, or a family member on payroll beyond their real role.

After those adjustments, our example practice lands near 392,000 dollars of adjusted EBITDA.

That is the number a buyer multiplies to reach an offer — and it sits more than 100,000 dollars above the net income on the P&L.

Why the rebuild matters to you

Two things follow. First, your net income understates your practice’s value to a buyer, often substantially, because it has not been normalized. An owner who quotes a value off net income usually leaves money on the table. Second, the rebuild is where most do-it-yourself valuations fall apart. We have watched general-purpose AI tools skip depreciation that was clearly labeled, miss owner-compensation normalization entirely, and return a confident number that was wrong by hundreds of thousands of dollars.

Adjusted EBITDA is not complicated once you see it built one line at a time, but it has to be built correctly. Every relevant line has to be found, and the owner-compensation normalization has to use real replacement rates. The same goes for the legitimate add-backs that separate the number on your tax return from the number a buyer will pay.

Practice Worth does this rebuild for you, line by line, and shows its work at every step so you can hand the report to your CPA or a buyer. There is a free sample report at getpracticeworth.com.

About the author. Dr. David Eslinger holds a DDS and an MBA and has spent more than a decade on the buy side of dental practice transactions, founding Eslinger Dental Consultants and holding C-suite, executive leadership, and board roles in the DSO industry. Karen Eslinger, RDH, co-founded Practice Worth in 2026. Practice Worth is a Missouri LLC. Learn more at getpracticeworth.com.

Karen’s companion piece reads the same statement from the chair side: reading your P&L the way a buyer does.