Buyers do not price the profit on your tax return. They rebuild it, and a big part of the rebuild is add-backs: spending that ran through the practice but was really owner benefit rather than a cost of producing the earnings. I covered the basics in the tax-return piece. This is the deeper cut, because in diligence some add-backs get accepted with a nod and others get laughed out of the room, and knowing the difference before you list is worth real money.

The three questions every add-back has to answer

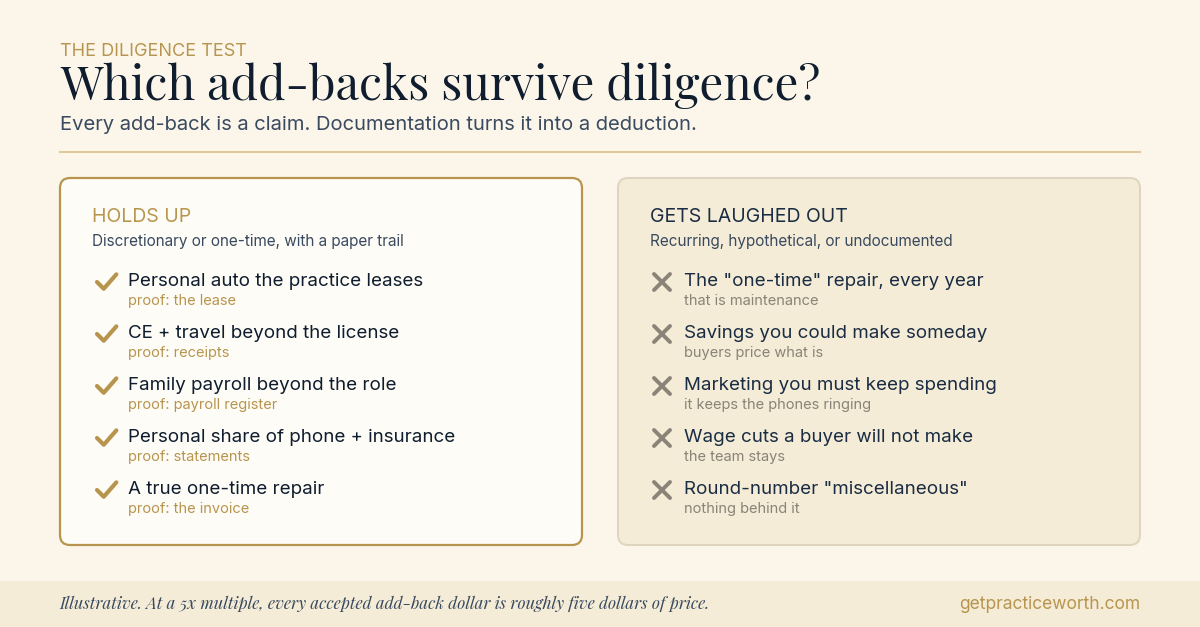

A defensible add-back passes three tests. Was the spending truly discretionary, or truly one-time? Would it disappear under a new owner without hurting the practice? And can you prove it with records a stranger can verify? An adjustment that misses any of the three is not an add-back. It is an argument, and arguments get priced at zero.

The ones that hold up

The reliable ones are familiar. The vehicle the practice leases that mostly drives to the lake house. Continuing education and the travel wrapped around it, beyond what your license actually requires. A family member on payroll whose duties would not survive a job interview. The personal share of your phone, insurance, and subscriptions. And true one-time costs, like the water-line repair after a flood or a legal matter that is settled and will not repeat. What these have in common is simple: none of them are needed to produce the earnings a buyer is purchasing, and each one leaves a paper trail. A lease, a payroll record, an invoice, a policy statement. (Owner compensation is a bigger and different animal, a two-step normalization rather than a simple add-back, and it has its own article.)

The ones that get laughed out

Then there is the other column. The “one-time” repair that shows up every single year; buyers call that maintenance. Hypothetical savings, as in “I could cut my lab bill twenty percent if I switched suppliers”; a buyer prices the practice you run, not the one you describe. Marketing spend you would have to keep spending to keep the phones ringing. Staff wage cuts a buyer will not actually make. And the round-number “miscellaneous” adjustment with nothing behind it. None of these survive an analyst who has your general ledger open in the next window.

Documentation decides it

Here is why the fight matters. At a five-times multiple, every accepted add-back dollar is roughly five dollars of price. Both sides know it, so a serious buyer’s diligence team ties each claimed add-back to the general ledger, line by line.

Documentation is the difference between a claim and a deduction.

If you can hand over the auto lease, the payroll register, and the credit card detail the day they ask, the adjustment holds. If you cannot, it quietly disappears from the buyer’s model, and your price goes with it.

Credibility compounds, in both directions

One aggressive add-back does more damage than the dollars involved. The analyst who catches it goes back through your clean items with sharper eyes, and adjustments that would have passed start taking haircuts. A conservative, documented schedule works the other way: the buyer starts extending your numbers the benefit of the doubt, diligence moves faster, and the offer that was made is the offer that closes.

Practice Worth builds your add-back schedule from the categories buyers actually accept, and it keeps the aggressive ones out of the math, so the number you take to market is one you can defend. The full framework is on the methodology page, and there is a free sample report at getpracticeworth.com.

About the author. Dr. David Eslinger holds a DDS and an MBA and has spent more than a decade on the buy side of dental practice transactions, founding Eslinger Dental Consultants and holding C-suite, executive leadership, and board roles in the DSO industry. Karen Eslinger, RDH, co-founded Practice Worth in 2026. Practice Worth is a Missouri LLC. Learn more at getpracticeworth.com.

Karen’s companion piece walks through where the defensible add-backs actually live: the owner perks hiding in your overhead.